Our Legal Blog

Your Resource For Legal Information

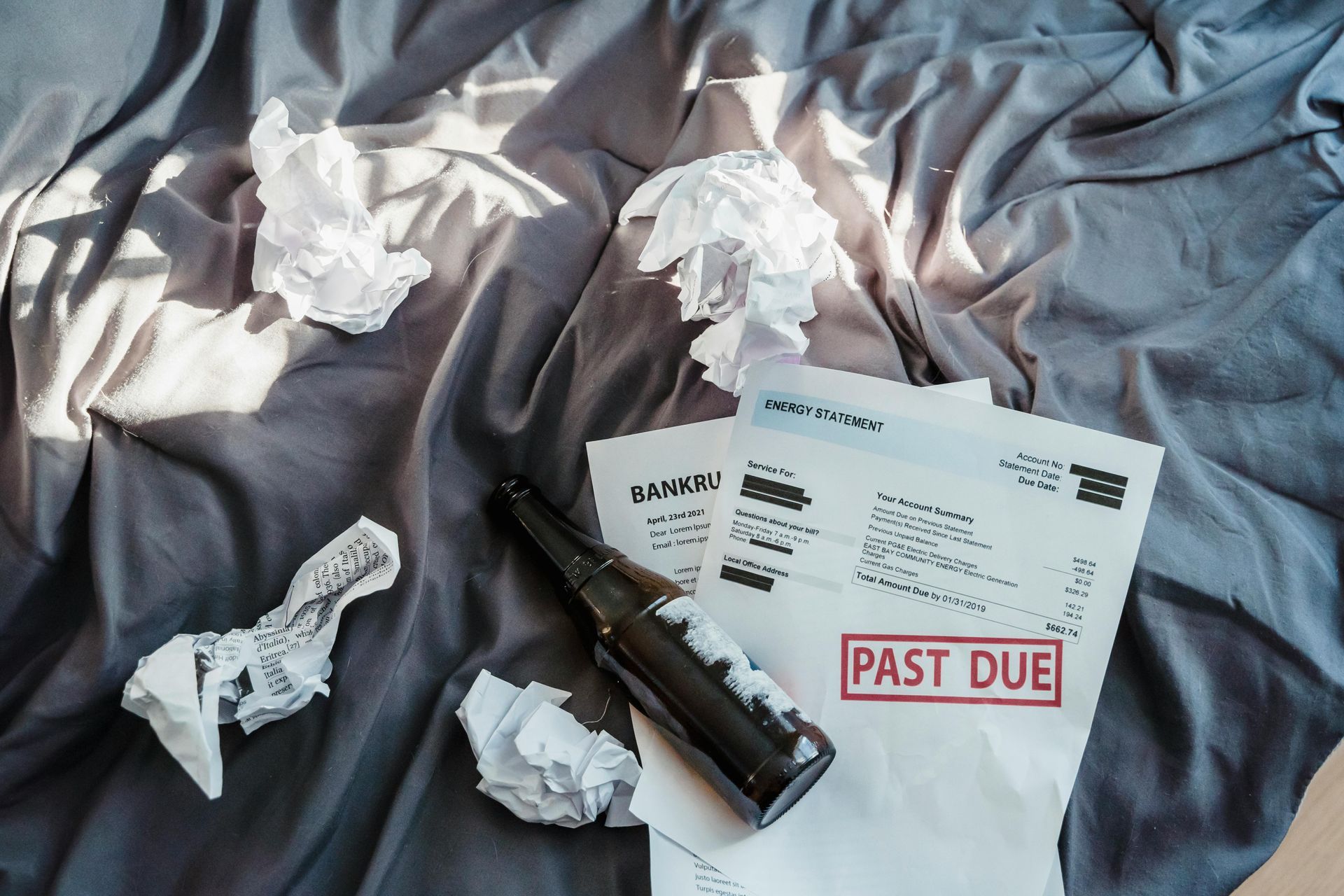

Learn how to qualify for Chapter 7 bankruptcy in Florida, including income limits, credit counseling, exemptions, and more. Serving Orlando residents at the Law Office of Paul L. Urich, P.A.

Filing bankruptcy involves several steps. While these steps are not specifically part of the bankruptcy filing, consumer credit courses are still required before the debt is fully discharged. Pre-filing credit counseling Before you can file for bankruptcy, you must complete this course. It aims to help you understand your financial situation and explore alternatives to bankruptcy. It must be taken from an approved agency, and you need to complete it within 180 days before filing. The course typically lasts about 60 to 90 minutes and can be done online, over the phone, or in person. During the course, a credit counselor will review your income, expenses and debts. They will help you create a budget and discuss possible options for managing your debt. If bankruptcy is the best option, the counselor will provide a certificate of completion, which you must include with your bankruptcy filing. Filing for bankruptcy Once you have completed the pre-filing credit counseling course and received your certificate, you can proceed with filing for bankruptcy. It involves submitting a petition to the bankruptcy court and various forms detailing your financial situation, assets, and debts. Post-filing debtor education After filing for bankruptcy, you must complete a debtor education course before your debts can be discharged. This course focuses on financial management and aims to help you avoid future financial problems. It covers topics such as budgeting, saving and using credit wisely. The debtor education course is also provided by approved agencies and usually lasts about two hours. Like the credit counseling course, it can be taken online, over the phone, or in person. You will receive a certificate upon completion, which you must file with the court to obtain your bankruptcy discharge. Importance of compliance It’s crucial to complete both the pre-filing credit counseling and post-filing debtor education courses. Failure to do so can result in dismissing your bankruptcy case, which means your debts are not discharged. These courses aim to ensure that you fully understand your financial situation and have the tools to manage your finances better in the future. A bankruptcy attorney can help with these other requirements Consumer credit counseling courses are a mandatory part of the bankruptcy process and serve an essential purpose. They help you assess your financial situation, explore alternatives to bankruptcy and learn how to manage your finances effectively. Completing these courses is essential for a successful bankruptcy filing and a fresh financial start.

When you’re overwhelmed by debt, bankruptcy may be your best option for a fresh start. In Florida, you must complete credit counseling before and after filing for bankruptcy. Pre-filing counseling helps you evaluate your financial situation and explore alternatives to bankruptcy. After filing, you must complete a debtor education course to have your debts discharged. These requirements ensure you’re making an informed decision and gaining financial management skills. Pre-bankruptcy counseling Pre-bankruptcy credit counseling involves a thorough review of your personal finances and a discussion about all available debt relief options, including bankruptcy. During this session, which typically lasts about an hour, you’ll work on creating a personalized budget plan. You can complete counseling in person, online or over the phone. Counselors charge around $50 on average but may reduce or waive fees based on your financial situation. After completing the course, you’ll receive a certificate that you must file with your bankruptcy petition within 180 days. Post-bankruptcy filing counseling After filing for bankruptcy, you must complete a debtor education course. This two-hour class covers budgeting, responsible credit use and money management. Like pre-filing counseling, you can complete this step in person, online or by phone. Counselors charge $50 to $100 but offer fee reductions based on your income. You must submit the completion certificate to the court before it will discharge your debts. Some people think you don’t need this step. However, if you fail to complete this course, the court can close your case without discharging your debts. You will then need to pay additional court costs and attorney fees to reopen your case. An experienced consumer credit counseling attorney can guide you through these requirements. They can help you find approved nonprofit counseling agencies and ensure you meet all necessary steps in the bankruptcy process. Working with a skilled and compassionate lawyer can lessen the complexities of bankruptcy law and help set you on a solid financial footing for the future.

Examining the pros and cons of Chapter 7 bankruptcy may help those struggling with debt in Florida to determine if it is the right solution for them. When people in Florida and throughout the U.S. are struggling financially, one of the options they may consider is filing for Chapter 7 bankruptcy. Although a valuable tool for helping individuals and couples get control of their debt so they can begin rebuilding their credit, declaring bankruptcy is not a step that should be taken lightly. Considering the benefits and disadvantages of filing Chapter 7. Pro: Relieve of financial obligations With few exceptions, a substantial portion of people’s debts may be discharged at the end of a Chapter 7 case. Therefore, they may be relieved of their financial liability for their qualifying obligations. These may include medical bills, credit card balances, past due rent or other money owed under lease agreements, certain civil court judgments and some personal loans, among other unsecured debts. Once debts are discharged, creditors can no longer take collection actions against people to attempt to recover any portion of them. Con: Property liquidation Before people receive a discharge in Chapter 7 bankruptcies, some of their possessions will be recovered by a court-appointed trustee and subject to liquidation. Upon filing a Chapter 7 petition, the bankruptcy trustee takes control of people’s estates. Their non-exempt assets, which may include extra vehicles, art collections and other property, may be sold or otherwise disbursed. The proceeds of the asset liquidation are then applied toward repaying all or a portion of their debts. Pro: Exemptions protect important assets While a number of people’s possessions may be subject to liquidation during Chapter 7 cases, exemptions allow them to keep many of their important assets. Such exemptions may extend to filers’ primary residences, vehicles under a certain value, and many of their home goods and personal effects. This may help ensure they are able to achieve a fresh start after coming through their cases, as they will not be left with nowhere to live, no transportation or other issues that might result if they were to lose all their property through a bankruptcy declaration. Con: Must qualify for approval Not everyone who seeks Chapter 7 protection is approved. Rather, people must meet a range of eligibility requirements, including the following: having a monthly income that is below the state’s average or qualifying under the means test, having no prior bankruptcy dismissals within the previous 180 days under certain circumstances and having completed credit counseling within 180 days of filing their petition. Pro: Resolved quickly Compared to other debt relief options, declaring Chapter 7 bankruptcy offers people an efficient resolution, allowing them to move forward with their credit and their lives. From filing their petitions until their cases are finalized generally takes between three and six months, provided there are no complexities or extenuating circumstances. Chapter 13 bankruptcies, on the other hand, take three to five years to complete.

Zombie titles result when banks do not complete foreclosures, leaving homeowners on the hook and potentially causing them further financial challenges. Financial challenges are a very real problem for many people in Orlando, and throughout Florida. Often, those who are struggling with overwhelming debt may have difficulties keeping up with their regular mortgage payments . As a result, some homeowners may be forced into foreclosure, or choose to leave their homes in an effort to avoid bankruptcy. Many who find themselves in this situation, however, are unaware of zombie titles and the dangers they hold. What are zombie titles? Often, when people receive foreclosure notices for their homes, they quickly move out. However, the bank may later dismiss the foreclosure. In these cases, the titles are never taken over by lenders and therefore remain in the owners’ names. These titles, then, are generally referred to as zombie titles. According to a National Mortgage News report, there are approximately 152,000 such homes across the U.S. It is very common that the owners of these properties are not aware that they still hold these so-called zombie titles. Lenders may not provide notice of cancelled foreclosures Even after starting the process, banks do not have to follow through with foreclosures. There are a number of reasons why a bank may choose not to pursue a foreclosure, or to cancel it altogether. Banks typically send out numerous notices regarding the initiation of the foreclosure process. However, they have no legal obligation to notify homeowners that the foreclosure process will not be pursued further, according to Forbes. For this reason, it is important for people to stay app rised of the situation, even if they have vacated their homes. Property tax liabilities Once a foreclosure has been started, many people believe the title is transferred over to the bank. That is generally not the case, however. As such, owners of zombie title homes remain liable for the property until the bank takes over possession or it is sold to someone else. This means that it is the owner, and not the bank, who is responsible for the home’s property taxes. Failing to pay property taxes, even on zombie title properties, may lead to wage garnishment or other legal actions. Foreclosures may carry unexpected expenses After an owner has vacated a property that is being foreclosed on, the home could fall into disrepair. Additionally, squatters and others may take advantage of the abandoned property and trespass. It is often the homeowner, not the bank, who is responsible for repairing any damages and maintaining a home during a foreclosure. Furthermore, the owner could be held liable if the property is in violation of city housing ordinances or codes. All of these things could lead to added fees, expenses and costs that already financially strapped homeowners may not expect. This could seriously impact owners’ credit and futures. They may have added debts, which could force them into an unwanted bankruptcy , or prevent them from moving on from their losses. Seeking professional legal counsel Receiving notice that their homes are being foreclosed on can be devastating for Florida families. In addition to forcing them out of their homes, foreclosures may also have an adverse impact on homeowners’ credit. These issues may be worsened in cases when people learn that the process was never completed and their home’s title has become a zombie title. In some cases, working with an attorney to seek bankruptcy protection may help people to avoid foreclosure. This may allow them to keep their homes and avoid becoming the victims of zombie titles. Keywords: bankruptcy, foreclosure

One of the most common New Year’s resolutions for Americans is related to their finances in some way – and more specifically, taking control of them. Some people resolve to track their spending more so they’re more aware of where their money is going. Others vow to use cash rather than credit cards. Still others promise themselves they’ll put some…

With the start of a new year, a lot of Americans are taking stock of their finances and looking for the best way to get out of debt. If your debt has become overwhelming and is affecting your ability to pay for everyday necessities, it may be time to consider bankruptcy. You wouldn’t be alone. Personal bankruptcies in the U.S.…

College students often find themselves navigating the challenging waters of financial independence for the first time. The combination of student loans, credit card debts, and everyday living expenses can quickly become overwhelming. Many students, eager to enjoy their newfound freedom, might not fully grasp the long-term implications of their financial decisions, such as high interest rates and the accumulating burden…

College students are facing increasing levels of credit card debt. On average, students carry over $3,280 in credit card balances. According to a 2024 study, roughly 65% of students have some form of credit card debt. This figure surpasses the amount of student loan debt, which also causes significant worry. In fact, 53% of students consider credit card debt their…

With summer winding down, now is a great time to review your finances. Many people accumulate debt over the summer, and addressing this before the end of the year can have significant benefits. What have I spent so far? Summer is a time for vacations, fun and sometimes unexpected expenses. Here are some common types of debt people accumulate: Vacation…